Declined Proposals

Please communicate the decision to the customer before appealing.

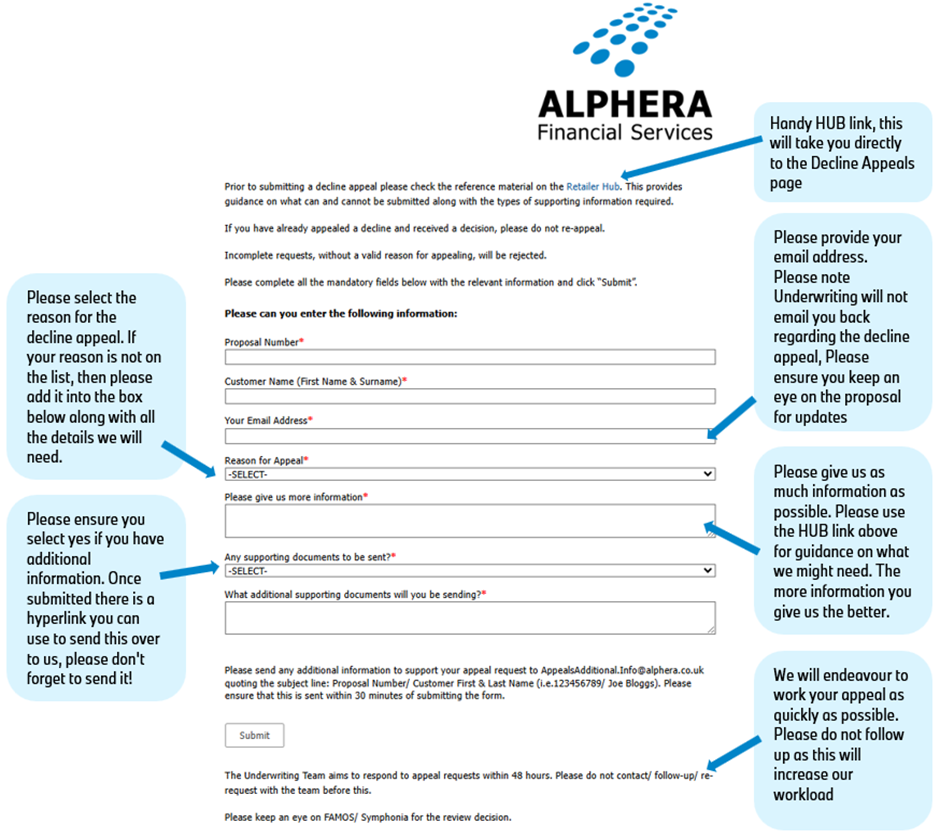

You can appeal a decline directly to our underwriting team via a new online form. To help underwriting review your case first time and promptly, please include any additional information requested alongside the form.

APPEALING YOUR DECLINE

When to appeal

- You have new information that supports the application and wasn’t provided at submission.

- The customer’s details were incorrect on the initial submission.

When not to appeal

- There’s no new supporting information to add.

- The customer has a weak credit file.

- The customer isn’t the main driver/keeper of the vehicle (this is outside of our terms and conditions).

- You or the customer have appealed the decline within the last 90 days.

Helpful information to include

- Verified income sources (e.g., pension, rental income, secondary employment).

- Recent promotions, pay raises, or new car allowances (verification required; attach relevant documents).

- Recent changes to the credit file not yet reflected (e.g., fully paid credit card balances).

- Explanations for any credit file discrepancies, supported by evidence.

- Any significant incorrect information from the initial submission.

Important notes

- Incomplete forms or missing information will delay the review, so please provide as much detail as possible to help the Underwriting team evaluate the decline.

- SLA and guidance: Underwriting will handle these new decline appeals as efficiently as possible, with an expected turnaround of up to 2 days. They’ll strive to shorten this where feasible. Please avoid follow-ups, as these can add to workload and delays.

- The decline page on the HUB will be updated soon with additional support to maximise the value of this new process.

How to Appeal

Use this link to submit your appeal: ALPHERA Underwriting Decline appeal

Please complete all fields and send any supporting documentation within 30 minutes of submitting the appeal to: AppealsAdditionalInfo@bmwfin.com. Include the subject line:

Proposal Number / Customer’s First & Last Name (e.g., 123456789 / Joe Bloggs).

Please note:

We aim to respond to decline appeals within 2 working days.

Before appealing, please note the decline term:

Proposals with unsupportive information seen at the Credit Reference Agencies are unlikely to get overturned.

We may not be able to review proposals declined for being too high risk, if there is other concerning information found that we are unable to share.

Customer Decline Appeals

If the customer is still not satisfied with the decision they are able to contact us with their own appeal with further justification via email on Customer.DeclineAppeals@bmwfin.com - please note there is no set template required for customer appeals.

(Please note we aim to respond to all customer decline appeals within 5 working days).

Information on Proposal Decline Reasons

"The Proposal has been declined based on a full review of the Businesses Financial Performance."

"We have declined this customer due to unsupportive information held against them at the Credit Reference Agencies. If the customer is unaware of the information, we strongly suggest that they obtain a copy of their credit file for all addresses where they have lived or applied for credit in the past 6 years. We are not in a position to reconsider this decision."

"The overall profile of this application is considered too high risk to approve. Information has been obtained from various sources, including credit reference and other agencies that prevents us from offering an approval. We are not in a position to reconsider this decision."

"This proposal has failed to meet our minimum Underwriting criteria. We are not in a position to reconsider this decision."

"Following a full review of the customer's credit file, we consider the applicant to be fully financially committed. We are not in a position to reconsider this decision."

"Thank you for supplying additional information for this customer. The information has been reviewed in full and is not deemed supportive of this application."

The company proposed is not supportive. Information will be taken from public records, such as Companies House and Credit Safe, as well as credit reference agency date.

The customer will have been declined due to adverse information. Such as account defaults, County Court Judgements and arrears on current pieces of credit.

This can be for a variety of reasons. Inaccuracies seen for the customer across their current financial agreements. The vehicle and lend is too ambitious (for example an 18 year old student looking for an X7) fraudulent information given or a fronted application.

A weak modest customer profile.

The customer is heavily using all available credit. Their credit cards are at or over limits, cash advances taken. Multiple loans and overdraft usage seen. If you have informed the underwriters of settlement this would be taken into consideration when making the decision.

The additional info such as bank statements, or tax return is not supportive. For reasons such as returned direct debits on bank statements, heavy use of planned or unplanned overdraft facility.

For tax returns this will be down to the declared income being too low to offer any type of lend.

Never miss a thing

Stay in touch with all the latest news and updates from ALPHERA and the motor finance industry, delivered direct to you.